Somewhere in India right now, a woman is closing out a quarter where the mutual fund she manages beat its benchmark. She did not take a big risk or make a flashy move. She read the numbers carefully, made calm decisions when calm decisions were needed, and won the way funds are actually supposed to be won: quietly. Somewhere else, at almost the same time, a man does the same thing, posts a similar number, and gets noticed for it. That difference, not in the result but in who gets seen for it, is one of the more telling patterns in modern finance.

This is not just a feeling. Researchers who track where money actually goes have measured it directly. Investors pay less attention to funds run by women than to funds run by men, and they react far more strongly to a man’s good month than to a woman’s identical one. The gap has nothing to do with performance. It has everything to do with who investors picture in the chair before they even look at the numbers. And once you do look at the numbers, they tell a very different story.

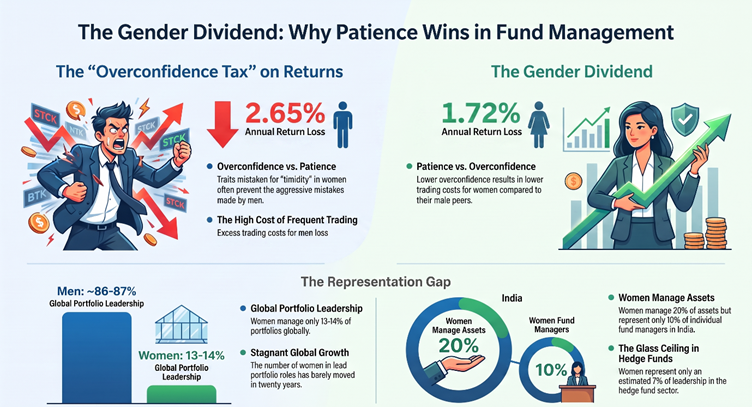

Start with the hard data, because it does not support the assumption. A Goldman Sachs analysis of the market’s recovery from the March 2020 crash found that 48 percent of female-managed funds beat the market in the months that followed, compared with just 37 percent of all-male-managed funds. Research from Investment Metrics on global large-cap equity portfolios found that in a tough year for markets, portfolios led or co-led by women lost far less against their benchmarks than portfolios run entirely by men. A separate study of 2,600 U.S. equity funds between 2008 and 2021 reached a blunter conclusion: all-male teams were the weakest performers in the entire group. In India, researchers studying local fund managers keep finding the same pattern, a more careful, risk-aware style that produces steadier returns, with less swagger and fewer wild swings.

That last point is the key to the whole story. The very trait people read as caution, even timidity, in a female fund manager is the same trait that saves her portfolio from the mistakes that keep tripping up her male peers. Overconfidence is not just a personality quirk. It is a cost, and men pay it more often. Studies on investor behavior have found that men trade more often and more aggressively than women, and that this extra trading hurts returns instead of helping them. One well-known study found that excess trading cost men about 2.65 percentage points a year in lost returns, against 1.72 points for women. Fund managers are not exempt from this just because they are professionals. The market does not reward confidence for its own sake. It rewards being right, and being right more often takes exactly the kind of patience that keeps getting mistaken for a lack of ambition.

So why does almost nobody know this? Part of the answer is representation. In India’s mutual fund industry, women manage close to a fifth of total assets, but they still make up only about one in ten individual fund managers. The global picture is similar. In recent years, only around 13 to 14 percent of active manager portfolios worldwide had a woman as lead or co-lead, a number that has barely moved in twenty years. In hedge funds specifically, one industry veteran put the figure at roughly 7 percent. The higher you climb in asset management, the fewer women you find, which means fewer women’s names come up in the rooms where reputations get built.

But representation is only the easier half of the answer. Researchers at Yale and Columbia ran a study that exposed something harder to accept. Investment professionals judged identical investment advice more harshly when a woman’s name was attached to it, even when the evaluators had every reason not to discriminate and full access to the same performance data. The bias held up even when the evidence was right in front of them. This is not a gap that better information will close on its own. It is a gap in what people are willing to believe once the information is already there.

Think about how a rational market would treat any other asset behaving this way. If a stock kept quietly beating its sector while investors ignored it out of habit, no analyst would call that a curiosity. They would call it a mispricing and buy the stock before everyone else caught on. Women fund managers are, by almost every piece of evidence available, exactly that kind of mispricing: underpriced, overlooked, and beating the benchmark anyway, quarter after quarter, largely unnoticed by the very industry whose job is to notice performance.

The case for putting more women in the room where investment decisions get made does not need a new argument. The argument already exists. It is sitting quietly in the performance data, filed away in a fund that beat its benchmark again last quarter, waiting for someone to actually read it.

The writer is an assistant professor at Rishihood University, Sonipat, Haryana. The views written in article is solely her independent research views.

{kind=link}